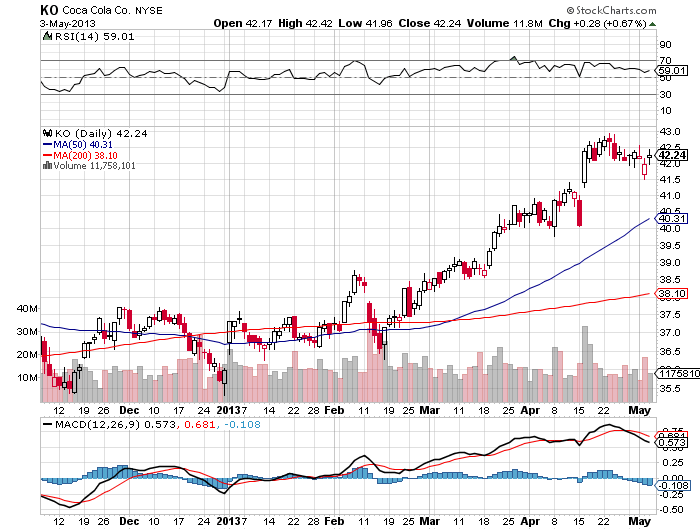

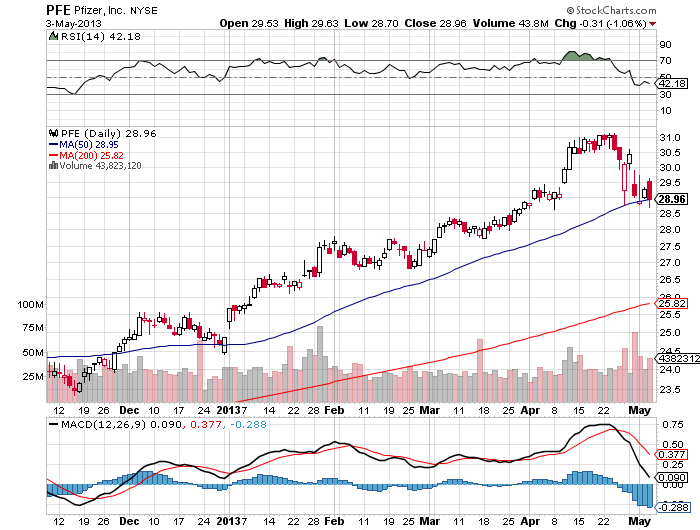

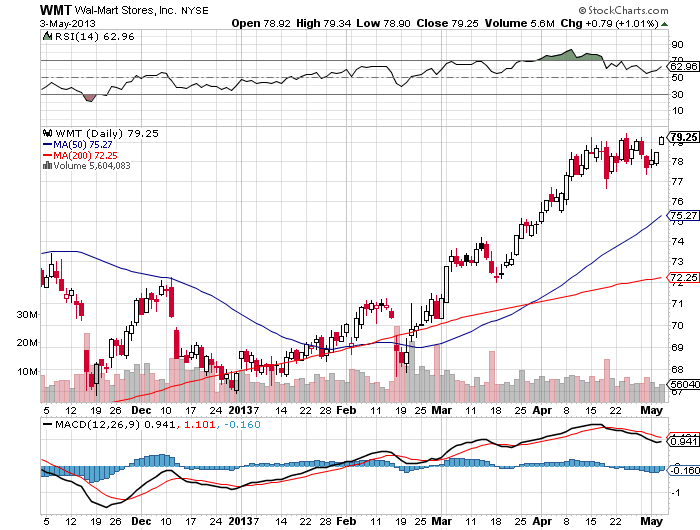

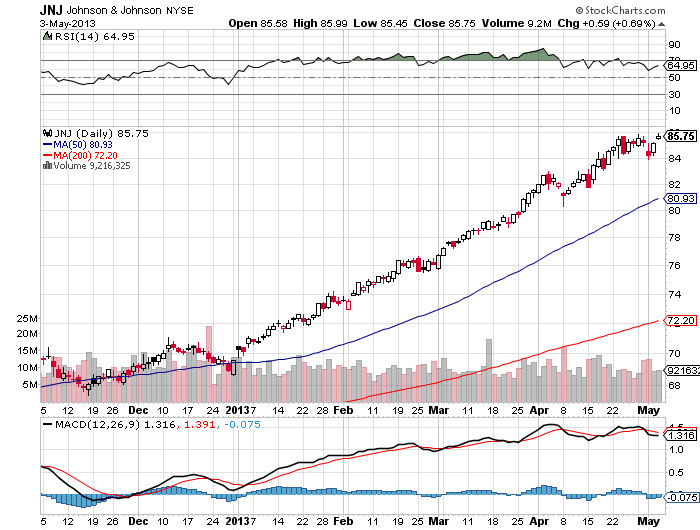

With the almost zero interest rates in place by the Federal Reserve, investors have been looking to blue chips and dividends as their main places to park their capital. This is why companies like Coca-Cola Company (KO), Wal-Mart (WMT), Pfizer (PFE) and Johnson & Johnson (JNJ) have been doing so well over the last six months to a year. This has happened because they're continually being forced out of bonds and cash into better-performing equities.

Here's how they've performed over the last year:

(click to enlarge)

(click to enlarge)

(click to enlarge)

(click to enlarge)

Recently the moved towards safer and better producing dividend companies has changed, as more and more capital is being allocated to the big tech sector, evidenced by upward moves in firms like Apple (AAPL), Microsoft (MSFT), Intel (INTC) and IBM (IBM). This began to happen from about April 15 to April 22.

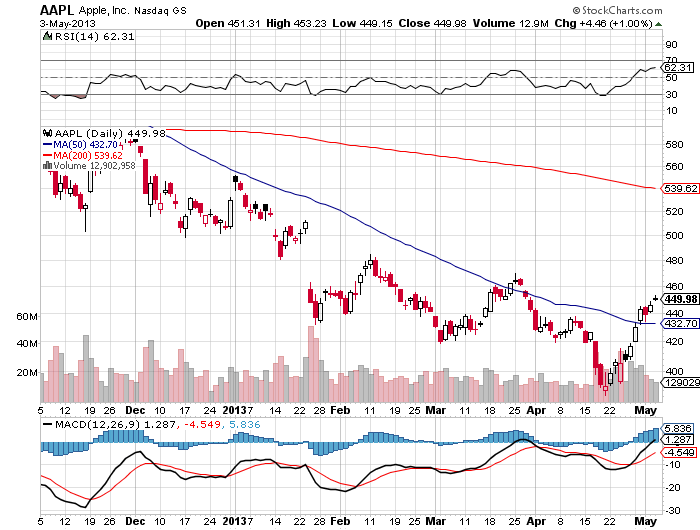

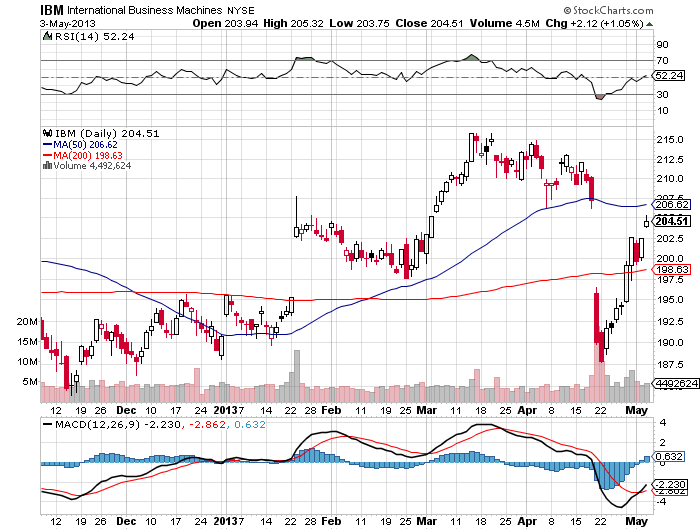

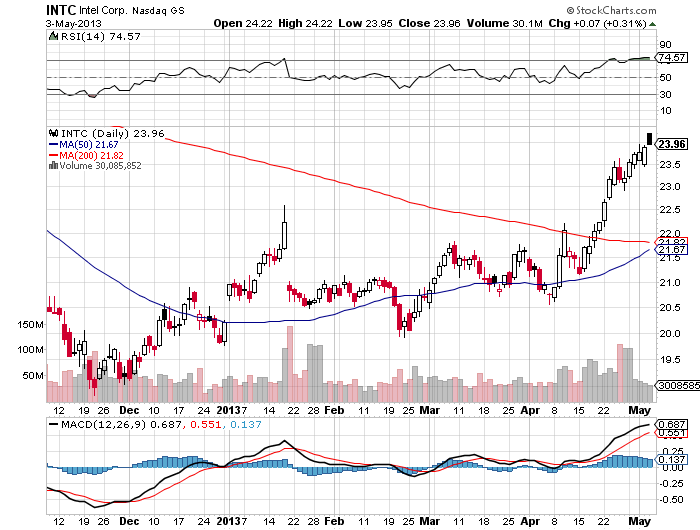

Below are the charts of these four tech companies to confirm they have started to move up in a way that looks sustainable.

(click to enlarge)

(click to enlarge)

(click to enlarge)

(click to enlarge)

I know that IBM, after its recent earnings report took a big hit, and is still below its 50-day moving average, yet it began to move in unison with the other big tech stocks, confirming there is definitely a more positive outlook for tech, as well as a growing risk appetite by main street.

That tells me investors, because of move up in dividend-paying blue chips, are ready to take on a little more risk, and the upward move in big tech stocks implies that's where their money is now headed. It also tells you they may believe the blue chips have soared so high they may not have a lot more room to run. They may have peaked. Either way, money is starting to migrate to big tech, and it looks like they're ready for a nice run.

Over the last couple of weeks the big tech stocks have been outperforming the blue chips, lending credence to my supposition. The only question appears to be if they will pull back some in the short term, or we've entered fully into the trend already. Whichever it is, big tech companies are close to rockin'.

Apple

Apple, as with all these companies have unique circumstances, but I'm going to use the tech giant as a bellwether for the overall big tech industry to unveil why they're overall poised for an upward, bullish trend.

There are two important elements to consider with Apple and all the big tech companies, and that is the current price levels and the net cash positions of the companies (cash on hand minus debt).

The numbers used in this article will obviously change, but if you want to know the net cash position of any company you're interested in investing in, subtract debt from cash on hand and you'll know the strength or weakness in that regard.

Current Price Levels and Value

As you can see from the charts above, the current price levels of big tech companies are very attractive in light of the Federal Reserve policies and macro-economic conditions, as well as the net cash positions of the stronger companies.

The best way to see the value in a company is via its price-to-earnings (P/E) ratio.

Consider the amount of cash on hand with the large tech companies, as that alters the way we should look at the price-to-earnings ratio of each company.

With Apple, which is flush with cash, it dramatically changes the P/E equation. When I was checking out Apple's net cash position, the market value of the company was close to $415 billion. Cash on hand at that time was about $137 billion. You subtract

that from the $415 billion and the company is trading at only 6.7 times future earnings. That's an incredible bargain, to say the least.

So there is the combination of incredibly cheap stocks at the beginning of a significant uptrend. The sector has everything going for it at this time, and that should drive the share price of the companies up in a big way. It appears this ride has just begun.

Other Tech Companies

There are a number of tech companies that fit under this trend umbrella, including Google (GOOG), Microsoft and Cisco (CSCO).

Google is the most expensive of these, with a forward price-to-earnings ratio of 12.7. It has a market cap of $273.6 billion as of this writing, with cash on hand of $48.1 billion.

Microsoft is much cheaper, with a forward price-to-earnings ratio of 8.1. It's market cap is $276.4 billion, with cash on hand of $68.3 billion.

Cisco's forward price-to-earnings ratio is a paltry 5.8. It's market cap is $111.5 billion, with cash on hand of $46.4 billion.

There are other companies, but these are all set for a nice boost in share price, and that appears to be a trend that will go on over the next 6 to 12 months, possibly even longer. The blue chip trend lasted for about a year or so, and if that's an indicator that can be trusted, the big tech trend could experience the same time frame.

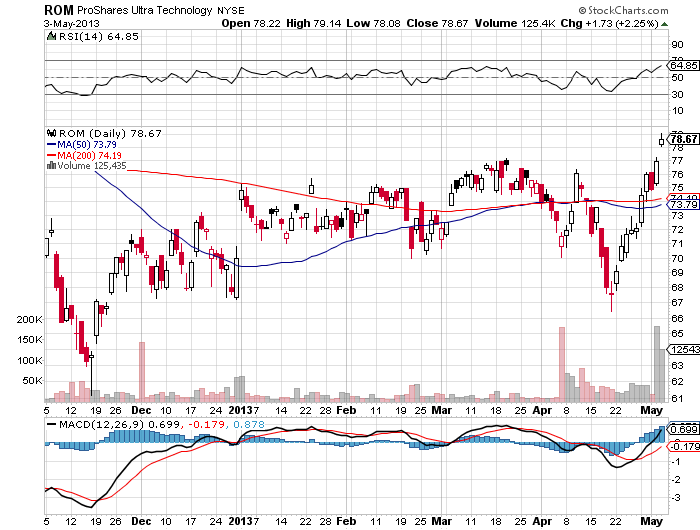

ProShares Ultra Technology (ROM)

One example of a technology ETF that will also do very well over the next year or so is ProShares Ultra Technology.

(click to enlarge)

Calculating the forward price-to-earnings ratio in the larger holdings of the fund, the average stands at only 11. That's also an amazing ratio, which bodes well for those investing in this and similar big tech ETFs.

(click to enlarge)

Unsurprisingly, ProShares Ultra Technology has moved in unison with the big tech stocks.

Conclusion

To me trends are the most important element in the share price movement of companies, as they will overcome all sorts of data and opposition when the trend takes hold. Trends defy logic, and can pull up even less attractive companies on momentum and sector favor.

That's what's happening in the big tech sector at this time, and we're just at the beginning of a big move.

Other than end-of-the-world scenarios, I don't see anything will stop this from going forward.

About the only risk I see is in when it'll happen. Is it possible there could be a temporary pullback? Absolutely. In that case it's a matter of hanging on if you're already in and waiting for the rebound.

The other possible risk is if this is a misreading of investment sentiment towards big tech. It doesn't appear to be, as the overall movement of the sector over the last couple of weeks is unlikely to be a fluke or anomaly, and so should be something

that takes hold to the benefit of those willing to invest in the sector.

As for Apple itself, the company will definitely rebound on the trend, but the lack of any known pipeline will eventually weigh again on the stock. In the meantime, it may not become a skyscraper in light of the existing conditions, but it will definitely go higher because of the current price levels and the big tech trend.

We are at the crux of this new trend, and while it may be a little early (maybe), it's very close to being time to get into the sector before it begins to soar.

Remember this is happening because of an increased risk appetite, attractive entry points, and low forward price-to-earnings ratios.

No comments:

Post a Comment